While “life expectancy” is a common term that most people use to denote the amount of time someone has left to live, technically, that is not what life expectancy means in the world of underwriting and life expectancy assessments. Life Expectancy or “LE” is actually the average number of months a member of a like-kind population of individuals can be expected to live. It is one point on a curve and more importantly it is not a point estimate. Life expectancy is a much more specific (and critical) concept for the purposes of a life settlement. As you’re well aware, having an individualized, accurate life expectancy assessment is critical to evaluating a life settlement correctly. Armed with the most complete information about micro-longevity risk, you can help your clients attract significant amounts of money for their life insurance policies. The need for more accurate life expectancy assessments, or LE reports, is vital for getting the highest values for life insurance policies. If you don’t want to leave money on the table, make sure that your LE report is as accurate as possible.

“What is in a life expectancy report from ISC Services?” you might ask. Our reports provide a projected life-span for an individual by evaluating mortality risk. Each report includes a specific mortality table and “Percent Probability of Death by Year” chart, in addition to more granular details, including medical impairments, lifestyle factors and functional status.

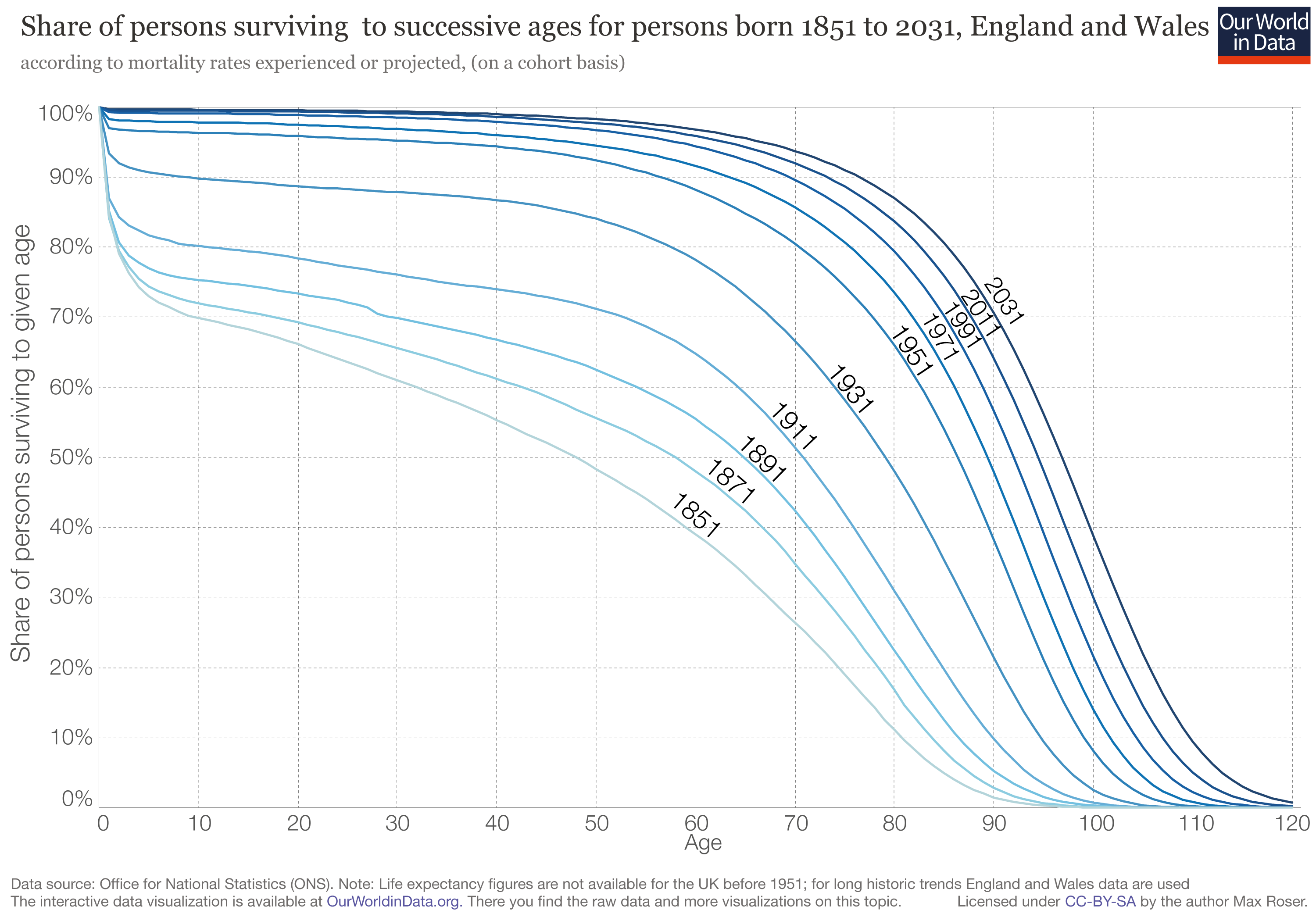

Generic online calculators will provide a life expectancy figure, but these rudimentary tools are useful for assessing your individual clients. The CDC provides mortality tables based on census data, but they barely scratch the surface of life expectancy assessment by calculating an average life expectancy for a large group of people of the same age and gender, known as macro-longevity data. The CDC tracks age, gender, and other demographic information and based on a particular birth year they provide a guess as to how long someone in the selected population group is likely to live on average. Called a cohort life table, mortality table or actuarial table, these simple models only look at age and gender. So if you’re looking for a very broad, ballpark answer to your longevity question, a generic table like this can help you find it. However, it can also be wildly inaccurate.

There’s another way to look at LE, however, and it’s far more applicable to the life settlement industry. You’ll want to evaluate LE based on your client’s individual health. You’ll want to consider their unique medical conditions, lifestyle behaviors and functional and social status factors all of which influence longevity. That’s why the best life expectancy calculators aren’t calculators at all. They are underwriters who leverage the most robust longevity assessment tools, apply experience-based training and insight, and consider a much wider range of factors. That’s where we come in.

How Do You Determine Life Expectancy?

At ISC we go beyond generic mortality tables to deliver the granularity you need to correctly evaluate life settlements for your clients and your business.

Our underwriters consider a wide range of information when producing a LE report, including but not limited to the following factors:

- Age

- Gender

- Address

- Citizenship Status

- Occupation or Past Employment

- Income & Net Worth

- Health Impairments

- Lifestyle Factors like Exercise, Tobacco, Alcohol, and Drug Use

- Functional Status

- Hobbies & Habits

As you might imagine, there is no one algorithm that can accurately and consistently evaluate all of these variables correctly. For 15+ years ISC Services has employed a sound, research-driven life expectancy underwriting process that produces individualized life expectancy assessments for life settlement companies. We assess the longevity risk associated with the specific insured in relation to a population of standard insureds of the same age, gender and smoking status. We use a proprietary process that blends the latest in longevity risk analysis tools with insights gained from over 80 years of professional experience in the underwriting industry. By marrying the science and the art of life expectancy assessment, we can provide you with consistent, well-reasoned LE reports that help you make the best decisions for your clients — something an algorithm just can’t achieve.

How Do Medical Records Impact Life Expectancy Reports?

So what is the life expectancy underwriting process like at ISC? Our approach involves a series of detailed steps, where we build a health and risk profile of each insured based on their specific data.

What Sets ISC’s Life Expectancy Reports Apart?

At ISC, we believe focusing on each unique individual is a crucial part of creating an accurate life expectancy assessment. Medical data and risk evaluation are just the beginning of an insured’s story. But it’s important to go beyond the basics and take the time to understand the individual people we assess by looking at more granular information and building a micro-longevity risk profile.

Since 2005, ISC Services has specialized in providing accurate life expectancy reports and scalable underwriting solutions using a sound, research-driven life insurance underwriting process. We offer individualized life expectancy underwriting and analysis specifically for life settlement companies. ISC’s LE reports are produced by our expert team of underwriters with decades of experience in assessing individual or “micro-longevity risk.”

{kind=link}